Investment Market Update

Global equity markets have remained relatively flat in March and April 2013. The volatility in the last two months has mainly revolved around continuing sovereign debt issues in Europe such and the Cyprus bailout. Some key themes affecting markets are as follows:

Australia

- The RBA (Reserve Bank of Australia) kept the official cash rate at 3% as Global economic conditions are showing signs of improving.

- Australian unemployment has increased to 5.6% (up 0.2%). This rate is expected to continue to increase slightly over 2013.

- Expectation of improved consumer spending and some general improvements in trading conditions for industrial stocks and banks have continued to drive the Australian share market up, with some small pull backs over March and April 2013.

- Many commodity prices have dropped during the month of April 2013, especially the gold price. This has resulted in resource share prices generally falling over the months of March and April 2013.

Europe

- Cyprus requested a bailout from the European Union. The initial proposal to tax all deposits was rejected and a revised package which protects deposits under €100,000 was approved. Cyprus accounts for less than 0.25% of Eurozone GPD, however investors feared the contagion, and speculated the Cyprus bailout could set a precedent for future bailouts.

- The Eurozone unemployment rate remained high at 12% (up 0.1% for the month) in February 2013. The manufacturing sector contracted further – the Eurozone PMI falling 1.1 to 46.8 in February (a figure less than 50 still signals contraction).

United States

- US economic growth for the quarter ending 31 March 2013 is forecast to be 2.5-3.0% pa. This is the seasonally adjusted rate.

- US company profitability is strong, benefiting from a competitive dollar, lower energy costs and historically high profit margins.

- The US jobless rate edged down to 7.7% (down 0.2% for the month) in February 2013.

- US housing market, as measured by the S&P/Case-Shiller House price index, rose at its fastest pace since 2006, at an annualised rate of 8.1% to January 2013.

- US Non Farm payrolls have consistently added nearly 200,000 jobs per month, on average, over the last 5 months (see chart below).

US Non-Farm Payrolls

Source: Datastream

China/Japan

- China’s manufacturing sector expanded in March 2013. The HSBC PMI (Purchasing Managers Index) was up 1.2 to 51.6 in March 2013 (more than 50 signals expansion).

- The Bank of Japan (BOJ) confirmed an inflation target of 2% pa. The Japanese are using a combination of quantitative easing (i.e. buying Government Bonds) and additional government spending to reinflate the economy. The Japanese share market has responded strongly to these initiatives.

Investment Market Performance

Selected Market Indicators Commentary for the Month ending 31 December 2012

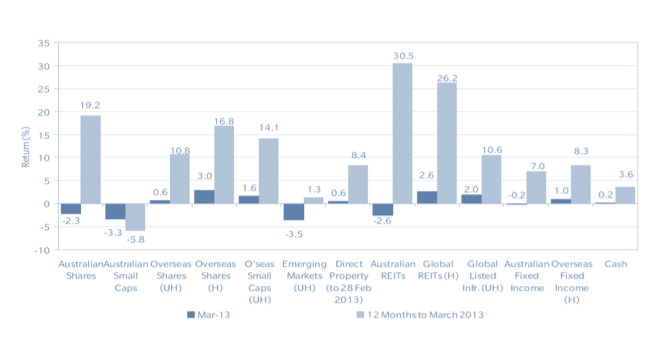

Asset Class Returns

Source: Thomson Financial Datastream; MSCI data provided ‘as is’

Australian Shares

After a few strong months, they Australian equity market fell in March with the S&P/ASX 300 returning -2.3%. This was primarily led by poor performances from the Resources sector (-9.6%) and the Energy Sector (-3.7%). Other sectors fared more favourably making small positive returns with Consumer Discretionary (+2.6%) and IT (+0.8%) being the strongest performing sectors.

Overseas Shares

Global equity markets had predominately positive returns for the month with the MSCI World (ex Aust.) Index rising +0.6%.

Most global sectors were up in March with the Healthcare Sector (+3.6%) and the Telecom Sector (+2.8%) being the strongest performers. The global Materials Sector experienced similar poor performance to the same sector in Australia and was the weakest global sector returning -4.4% for the month.

US stocks performed particularly strongly despite federal budget cuts and the potential for additional fiscal tightening forecast to occur during the year. The US S&P 500 returned +3.8% for the month, representing its highest monthly return since 2007.

European markets experienced generally small, but positive returns. The UK FTSE100 (+1.3%), French CAC 40 (+0.4%) and German DAX 30 (+0.7%) were all up in March.

Asian Markets were mixed with the Japanese TOPIX strongly up +7.0%, while the Chinese Shanghai Composite Index performed poorly, down -5.5%.

Property

Real Estate Investment Trusts (REITs) were mixed in March with Domestic REITs down -2.6% and Global REITs up +2.6%.

Fixed Interest

Global sovereign bond yields fell in March across the board with 10 year bond yields falling in the US (-4 bps to 1.85%), the UK (-20 bps to 1.76%) and Germany (-11 bps to 1.28%) experiences the biggest falls.

In contrast, Australian Sovereign bond yields rose over the month with the UBS Treasury Bond Index returning +0.2% in March.

Australian Dollar

The Australian dollar rose against all major currencies in March. The A$ appreciated +1.8% against the US$, making up for the loss experienced in February, and finishing the month of March at a value of US$1.043. The A$ also appreciated against the Yen (+3.8%), the Euro (+3.7%), and the Pound Sterling (+1.8%).

Leave A Comment

You must be logged in to post a comment.