Director’s Perspective

By Mario Isaias

The GFC was the trigger point for governments to embark on massive spending without finding new sources of revenue. Australia now faces the hard reality that this cannot go on forever. The upcoming Federal Budget on 13 May will most likely take the first steps to addressing this imbalance which will probably mean higher taxes and lower government spending. At Harvest, we will analyse the Budget that evening and send our annual Federal Budget Newsletter to you around midnight. Some good investment news however in March with the Australian stock market reaching a six year high before falling away by month end. Despite events in Ukraine, overseas markets have provided positive news with the Euro-zone now having positive overall GPD growth, China GDP still growing at over 7% and US unemployment heading towards 6.5%. We hope these positives will outweigh negative sentiment in the run up to 30 June so that investments returns are strong this financial year & superannuation/pension accounts show good growth.

Regional Commentary

Australia

Monetary policy – the Reserve Bank of Australia (RBA) left the cash rate unchanged at 2.5% at their April 2014 meeting for the seventh consecutive month. We believe the RBA is likely to continue to keep the cash rate on hold for the moment.

Retail – According to Australian Bureau of Statistics data released during March, Australian retail sales grew by 0.2% in the month of February 2014 revealing that consumer sentiment is beginning to improve.

Employment – Employment increased in the Australian economy by 18,100 in March 2014. However, despite this, the unemployment rate remained steady at 5.8%.

United States

Growth – The official US annual GDP growth rate for the December 2013 Quarter was revised up to an annual rate of 2.6% after previously being estimated at 2.4%.

Manufacturing – The ISM Manufacturing PMI rose to 53.7 in March, up from 53.2 during the previous month.

Monetary policy – The US Federal Reserve is expected to announce a further reduction of $10 billion per month to its monthly asset purchase programme, decreasing the monthly asset purchase rate from $55 billion to $45 billion, after its April/May meeting on 30 April 2014.

Employment – The US unemployment rate remained unchanged at 6.7% for the month despite creating 192,000 new jobs, while the participation rate increased 0.2% to 63.2%.

Europe

Manufacturing – Eurozone manufacturing slowed slightly in March with the Index falling to 53.0 (down from 53.2 in the previous month).

Inflation – The European Central Bank (ECB) left rates on hold at 0.25% for the month despite the fact that the inflation rate within the Eurozone fell to 0.5% pa in March 2014. This is well below the ECB’s target of around 2% and the EBC has indicated that it may look to cut interest rates in the future if conditions do not improve.

Employment – The official Eurozone rate of unemployment was 11.9% in February 2014. It has been steady at this rate since October 2013. Unemployment rates across the Eurozone are spread between Austria (at 4.8%) and Greece (at 25.6%).

China/Japan

Growth – The Japanese annual GDP growth rate came in lower than expected for the December 2013 quarter at 1.0%.

Manufacturing – Chinese manufacturing continued to weaken in March with the HSBC China Manufacturing PMI falling to 48.0 in March, down from 48.5 in February.

Inflation – Chinese inflation remained low throughout March 2014 with the Chinese consumer price index rising by 2.3% in the year to 31 March 2014.

Commodity Prices

Commodity prices were generally stronger during February 2014. The Oil price was up 1.2% to $109.29/bbl, Gold prices were also up 6.7% to US$1,325.70/oz. Iron Ore prices were the notable exception, dropping 6.3% to US$119.00/MT, which is a 7 month low.

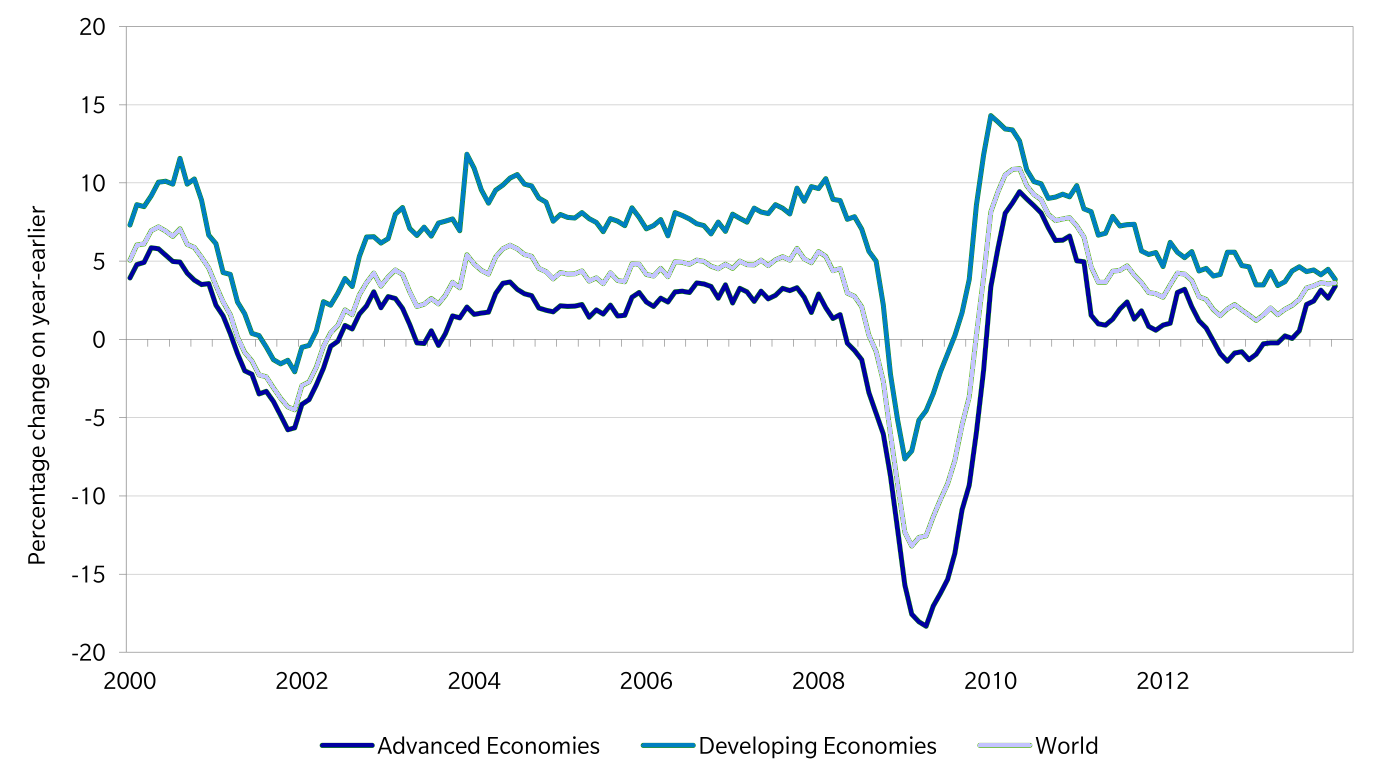

Global industrial production is trending up in advanced economies

As at 31 March 2014

Source: Netherlands Bureau of Economic Policy Research

Asset Class Returns for Selected Market Indicators

As at 31 March 2014

Source: Thompson Financial Datastream; MSCI data provided ‘as is’. Prepared by Harvest Financial Group.

Selected Market Indicators Commentary

For the Month Ended 31 March 2014

Australian Shares

The Australian share market was up in March returning +0.2% on the back of better than expected profit results revealed during the recent company reporting season.

The best performing sectors for the month of March 2014 were Financial ex. Property (+3.1%), Telecommunications (+0.8%) and Information Technology (+0.5%). The weakest performing sectors were Materials (-3.2%) and Consumer Staples (-2.1%).

Global Shares

Global share markets were generally down in March 2014 with the MSCI World (ex. Australia) Index falling -3.4% on an

un-hedged basis on the back of excessive valuations in the United States.

The strongest performing global sectors for the month were Utilities (-1.0%) and Energy (-1.4%). The weakest performing sectors in March 2014 were Consumer Discretionary (-5.6%) and Healthcare (-5.2%).

Markets in the U.S. were mixed in March 2014 with the expectation that the U.S. Federal Reserve would announce a further $10b per month taper to it’s bond buying programme. The NSADAQ was down -2.5% while the U.S. S&P 500 Composite Index was up by a modest +0.8% for the month.

European Markets followed the global trend and were generally down in March. Investors continued to show concern over the rising geopolitical tensions between the Ukraine and Russia with Western nations imposing trade sanctions on Russia after it completed its absorption of Crimea into the Russian Federation. Markets in the UK (-2.6%), France (-0.2%) and Germany (-1.4%) were all down for the month.

Asian markets were mixed during the month of March with markets in India (+7.6%) being the strongest performing while Hong Kong’s Hang Seng (-2.7%) performed the weakest.

Property

Domestic Real Estate Investment Trusts (REITs) were down in March 2014 returning -1.6%, while global REIT’s were up, gaining +0.2% on a fully hedged basis.

Fixed Interest (Bonds)

Global sovereign bond yields were up in March with 10 year bond yields rising in the UK (+2bps to 2.74%), the US (+6bps to 2.73%) and Germany (+4bps to 1.57%) over the month.

Australian bond yields were up in March 2014 with 10 year bond yields rising +7bps to 4.08%, while Australian 5 year bond yields were up +15bps to 3.44%.

Australian Dollar

The Australian dollar generally appreciated against other major currencies in March 2014. The A$ rose 3.1% against the US$, finishing the month at US$0.922. The A$ also appreciated against the Euro (+2.7%) and the Pound Sterling (+3.4%).

Click Here to download a PDF of this Newsletter

Leave A Comment

You must be logged in to post a comment.