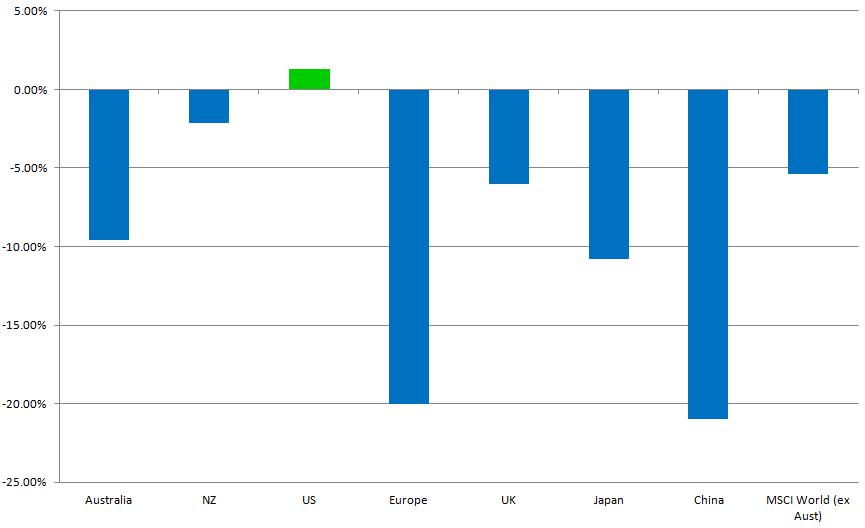

The last financial year has been a disappointing one for both global and Australian shares. For the 12 months to 30 June 2012, global shares returned -5.4% (MSCI World (ex Aust) $A; source: AMP Capital Markets), while Australian shares again underperformed global shares returning -9.6% (S&P/ASX200 Accum Index; source: AMP Capital Markets) over the same period.

Global share market performance to 30 June, 2012

Australian real-estate investment trusts performed far stronger for the year, returning +5.5% (S&P/ASX300 Property; source: Mercer).

Fixed income investments proved to be the strongest asset class with Australian fixed interest returning a very healthy +12.4% (UBS Composite Bond; source: Mercer) and global fixed interest delivering gains of +11.7% (Citigroup WBG hedged (ex Aust); source: Mercer).

Why have share markets performed so poorly in 2011/12?

Global economic issues, particularly concerns relating to the European Debt Crisis have been the primary contributors to poorly performing equity markets around the world.

In particular, concerns about Greek political instability and a possible exit from the euro due to sovereign debt issues, as well as the downgrading of America’s credit rating, caused significant damage to global markets early in the financial year. This was when most of the damage was done. Indeed, the signs of global equity markets recovering are being felt already with markets making small, yet positive returns in the last six months of the financial year. Unfortunately, these gains were not enough to overturn the damage done at the start of the year. The signs however, are more positive heading into the 2012/13 financial year.

Why were Australian shares weaker than global shares?

There are three main reasons for Australian shares underperforming global shares. Firstly, relatively high interest rates in Australia have made bank term deposits an attractive place for Australians to keep their money, resulting in less investment in shares and property. Secondly, the high Australian dollar has resulted in lower than expected earnings for companies that rely heavily on exports to generate profits. Finally, worries about the demand from China for Australia’s resources have lowered commodity prices and resulted in lower overseas investment in Australian companies.

Outlook into 2012/13

Global – Global business conditions suggest that global growth is likely to remain low in the immediate future. However, global growth should still remain above previous lows and we should see a continuing global recovery; albeit at a slow pace. Although short term volatility will remain high, cheap shares and easing monetary conditions should see share markets remain positive over the next 12 months.

Australian – The cash rate in Australia has fallen to 3.5% and is likely to fall even further, given the low inflation level, as the RBA attempts to entice people and businesses to spend more. Bank deposits will become less attractive as rates fall – which should free up capital to be invested in other asset classes (such as shares). Low share prices and high dividend yields will further encourage investors to invest in shares. Many economists expect the Australian dollar to fall somewhat, which should return some of the profits to export based companies, making them more attractive to investors. Australian shares are trading at historically low price to earnings ratios and this should see the outlook for Australian shares remain positive over the next 12 months.

GENERAL ADVICE WARNING © 2012 Harvest Financial Group Pty Ltd. This Newsletter has been prepared for clients of Harvest. This document contains confidential and proprietary information of Harvest Financial Group (‘Harvest’), and is intended for the exclusive use of the recipient to whom it is addressed. The document, and any opinions on investment products it contains, may not be modified, sold or otherwise provided, in whole or in part, to any other person or entity without Harvest’s prior written permission. Information on investment management firms contained herein has been obtained from the firms themselves and other sources. While this information is believed to be reliable, no representations or warranties are made as to the accuracy of the information presented, and no responsibility or liability, including for consequential or incidental damages, can be accepted for any error, omission or inaccuracy in this report or related materials. Opinions on investment products contained herein are not intended to convey any guarantees as to the future investment performance of these products. In addition, past performance cannot be relied on as a guide to future performance. This information has been sourced from Harvest’s independent research house Mercer Investment Consulting Research and other sources.

Leave A Comment

You must be logged in to post a comment.